Form 121 Replaces 15G and 15H: TDS Self-Declaration Guide

Jaspal Singh

Author

Last updated: 6 May 2026

Forms 15G and 15H Are Gone — Meet Form 121

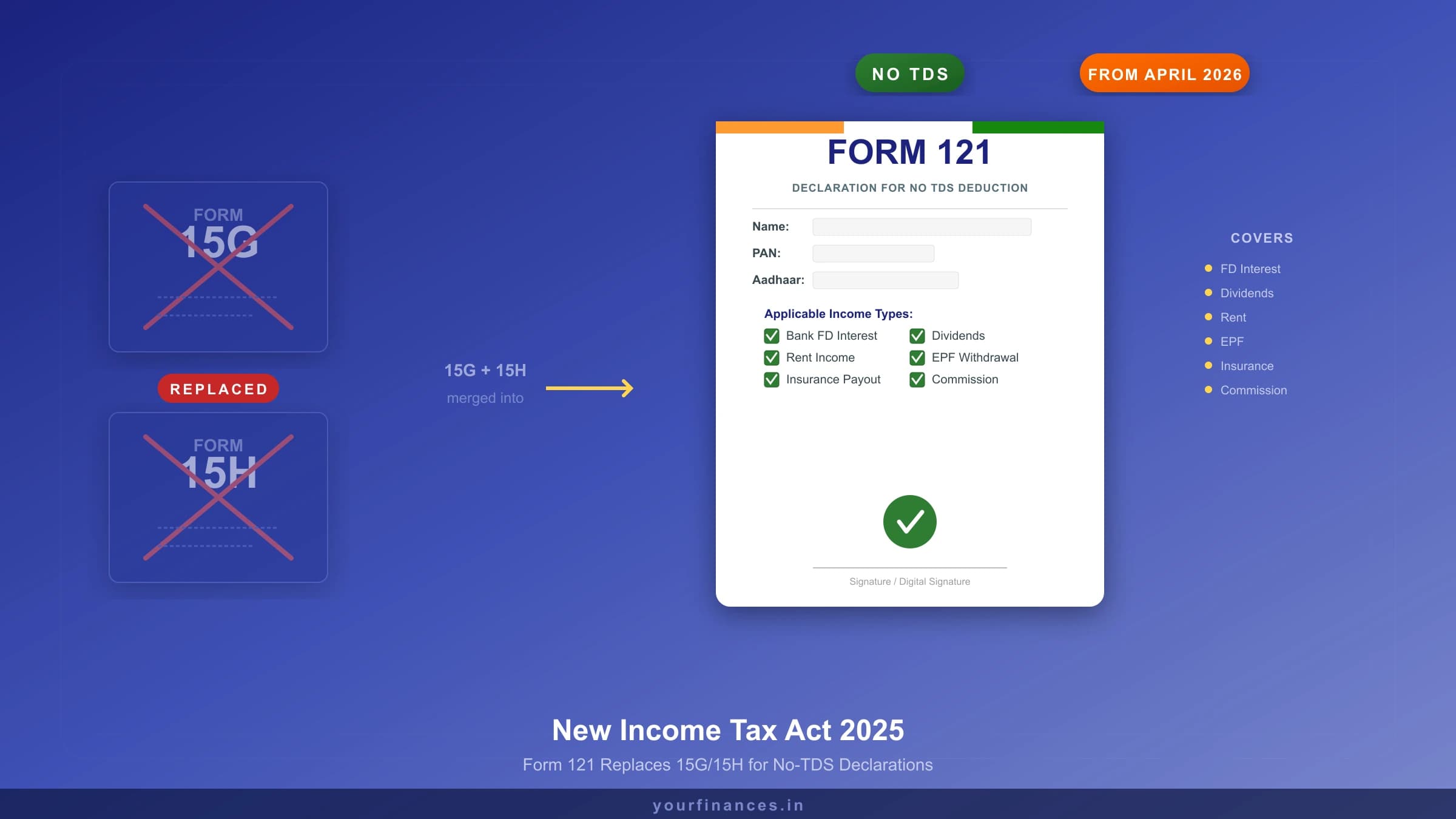

If you’ve ever submitted Form 15G or Form 15H to your bank to avoid TDS on your fixed deposit interest, you need to know this: those forms no longer exist.

From April 1, 2026, the new Income Tax Act 2025 has replaced both with a single, unified form called Form 121. Whether you’re 25 or 75, there’s now just one form for everyone.

This is one of the simplest but most impactful changes in the new tax law. Here’s everything you need to know.

What Is Form 121?

Form 121 is a self-declaration you submit to a payer (like your bank, post office, or tenant) to tell them: “My total income for this year is below the taxable limit, so please don’t deduct TDS.”

It works exactly like the old Forms 15G and 15H did — but now it’s one form for all eligible taxpayers, regardless of age.

Why Did This Change?

Under the old system, people under 60 had to file Form 15G, while senior citizens (60+) filed Form 15H. Same purpose, different forms. This caused confusion, wrong form submissions, and rejected declarations. Form 121 eliminates all of that.

Who Can File Form 121?

Eligible

- Resident individuals — any age (below 60, senior citizens 60+, super seniors 80+)

- Hindu Undivided Families (HUFs)

- Other specified entities meeting the criteria

Not Eligible

- Companies and firms

- Non-resident Indians (NRIs)

- Anyone whose estimated tax liability is not zero

The key condition remains the same: your estimated total income for the tax year must result in zero tax liability. Under the new tax regime, this means income up to ₹12 lakh (thanks to the Section 87A rebate).

What Income Types Does It Cover?

Form 121 prevents TDS deduction on a wide range of income types:

| Income Type | Common Example |

|---|---|

| Interest on deposits | Bank FDs, RDs, post office deposits |

| Dividends | Dividend from shares and mutual funds |

| Rent | Rental income from tenants |

| PF withdrawals | EPF withdrawal before 5 years |

| Pension | Monthly pension payments |

| Insurance commission | Commission earned by insurance agents |

| Life insurance payouts | Maturity proceeds of certain policies |

| Mutual fund income | Redemption proceeds, dividends |

The most common use case remains the same as before: stopping TDS on FD interest. If your total income is below the taxable limit, your bank shouldn’t be deducting tax on your interest — and Form 121 ensures that.

Use our FD Calculator to check your expected interest income for the year.

How to File Form 121: Step by Step

- Check your eligibility — Will your total income for the tax year result in zero tax? If yes, you qualify.

- Download the form from the Income Tax Department website or your bank’s portal.

- Fill in your details — Name, PAN (mandatory), residential status, estimated total income, and the income on which you want TDS exemption.

- Submit to each payer separately — If you have FDs in 3 banks, you need to submit Form 121 to each bank individually.

- Submit before the income is credited — You must file it before the bank credits your interest, not after.

- Keep a copy for your records.

Important: You can submit online (if your bank offers it) or as a physical paper form at the branch.

The New UIN System

One of the smartest upgrades in Form 121 is the Unique Identification Number (UIN) system.

When your bank receives your Form 121, they assign it a UIN that contains:

- A sequence number

- The relevant tax year

- The payer’s TAN (Tax Account Number)

This UIN is then quoted in the bank’s quarterly TDS statement (Form 140), making it easy for the Income Tax Department to track and verify every declaration. No more mismatches or lost forms.

Key Deadlines

| Action | Deadline |

|---|---|

| Submit Form 121 to payer | Before income is credited/paid |

| Payer uploads monthly statement | By 7th of the following month |

| Payer files quarterly TDS return | Along with Form 140 |

Pro tip: Submit Form 121 to your bank at the start of the financial year (April itself) to ensure no TDS is deducted from your very first interest payment.

Form 121 vs Old Forms 15G/15H

| Feature | Old System (15G/15H) | New Form 121 |

|---|---|---|

| Number of forms | Two (15G for under 60, 15H for 60+) | One unified form |

| Age-based selection | Yes — had to choose correctly | No — one form for all ages |

| Tracking system | Manual, error-prone | UIN-based digital tracking |

| Smart features | None | Auto-population, validations, API integration |

| Applicable law | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Effective from | Until March 31, 2026 | April 1, 2026 onwards |

Common Mistakes to Avoid

- Filing without PAN: Your declaration is invalid without a valid PAN. The bank will deduct TDS at the higher rate of 20%.

- Submitting after interest is credited: Form 121 must be submitted before the income is paid or credited. Late submissions won’t stop TDS already deducted.

- Filing when your income exceeds the limit: Form 121 is only for those with zero tax liability. Filing falsely can attract penalties under the Income Tax Act.

- Submitting to only one bank: You need to file separately with each payer — each bank, post office, or tenant.

- Thinking it exempts you from tax: Form 121 only prevents TDS deduction. If your income turns out to be taxable, you still owe tax when filing your return.

Other New Tax Forms You Should Know About

Form 121 isn’t the only change. The new Income Tax Act 2025 has overhauled several forms:

| Old Form | New Form | Purpose |

|---|---|---|

| Form 16 | Form 130 | Salary TDS certificate from employer |

| Form 15G/15H | Form 121 | TDS exemption declaration |

| Form 26AS | Form 155 | Annual tax statement |

| — | Form 123 | Perquisites and fringe benefits (new) |

| Form 140 | Form 140 | Quarterly TDS statement (retained) |

If you’re a salaried employee, the biggest change for you will be Form 130 (replacing Form 16), which your employer will issue from June 2027 for Tax Year 2026-27.

Who Should File Form 121 Right Now?

If any of these apply to you, submit Form 121 to your bank this month:

- Retirees and senior citizens with FD interest as primary income, where total income is below ₹12 lakh

- Homemakers with FDs in their name earning interest above ₹40,000/year

- Students or young earners with savings accounts or FDs but no taxable income

- Anyone earning below the taxable threshold who receives interest, rent, dividends, or pension

Use our Tax Calculator to check whether your total income results in zero tax liability under the new regime.

The Bottom Line

Form 121 is a welcome simplification. One form instead of two, a smart UIN tracking system, and the same fundamental purpose: preventing unnecessary TDS when your income is below the taxable limit.

If you used to file Form 15G or 15H every year, just switch to Form 121. The process is nearly identical — the form name and number have changed, but the idea hasn’t. Submit it to your bank early in April and you won’t lose a rupee to unnecessary TDS all year.

Frequently Asked Questions

What is Form 121 in income tax?

Form 121 is the new unified TDS self-declaration form introduced from April 2026. It replaces both Forms 15G (for non-senior citizens) and 15H (for senior citizens). It allows you to declare that your total annual income is below the taxable threshold so banks/payers don't deduct TDS on your interest income.

Who can file Form 121?

Indians whose total income is below the basic exemption limit (₹2.5 lakh for non-seniors, ₹3 lakh for seniors above 60, ₹5 lakh for super-seniors above 80). Both individuals and Hindu Undivided Families (HUFs) can file. NRIs cannot file Form 121.

What is the difference between Form 121 and Forms 15G/15H?

Form 121 unifies what 15G and 15H did separately. Single form, single PAN-linked declaration. The eligibility thresholds remain the same — based on total annual income. The biggest change: Form 121 supports digital filing through bank apps, eliminating paper forms.

How do I file Form 121?

Three routes: (1) Bank/AMC online portal — most banks now have Form 121 in their net banking; (2) Income Tax e-filing portal — register on incometax.gov.in and file electronically; (3) Bank branch — submit physical form for those without digital access. The form must be filed before the first interest credit of the financial year (typically April).

What income types does Form 121 cover?

Form 121 covers: bank FD interest, RD interest, dividend income, EPF withdrawal interest, savings account interest above ₹10,000, post office FD/SCSS interest, debenture/bond interest, and rental income. Salaries are not covered (employer handles TDS based on Form 16).

What happens if I don't file Form 121?

The bank/payer will deduct TDS at the prescribed rate (typically 10% for residents, 20% for non-PAN holders). You can claim a refund when filing your ITR — but the money is locked with the government for 6-15 months. Filing Form 121 timely avoids this lock-in.

How is Form 121 different for senior citizens?

Senior citizens (60+) get higher exemption thresholds — ₹3 lakh basic exemption + ₹50,000 specifically for FD interest under Section 80TTB. Super-seniors (80+) get ₹5 lakh basic exemption. Form 121 has senior-specific fields to capture these. Senior citizens may also be eligible for partial TDS waivers.

Can I file Form 121 if I have multiple bank accounts?

Yes. Form 121 is filed at each bank/AMC where you have FDs/RDs. The same PAN-linked declaration applies across all institutions. However, you must aggregate income from all sources when calculating eligibility — banks may cross-verify via PAN.

When should I file Form 121 each year?

File at the start of every financial year, ideally before the first interest payment. For most banks, this means before April 30. Late filing means TDS is deducted on early interest payments — refund possible only via ITR. Re-file annually as eligibility may change.

Is Form 121 mandatory?

No, it's voluntary — a self-declaration to avoid TDS. If you're comfortable having TDS deducted (and claiming refund later), filing isn't required. But for retirees and low-income individuals, filing saves cash flow and reduces the wait for tax refunds.

Disclaimer: This article is for educational purposes only and does not constitute tax advice. Please consult a qualified tax advisor or chartered accountant for advice specific to your situation.

Related Guides

- How to Withdraw PF Online — how TDS applies to EPF withdrawals and when a Form 121 / 15H declaration can prevent it.

- Senior Citizen Savings Scheme (SCSS) Guide — where senior-citizen TDS self-declarations matter most.

- Best FD Rates in India — compare the latest fixed-deposit rates before you lock in.

Written by

Jaspal Singh

Founder & Editor

Personal finance writer helping Indians make smarter money decisions through clear, jargon-free guides on taxes, investments, and budgeting.

Continue Reading

Belated & Revised ITR: Deadlines & Penalties

Missed the ITR deadline or made a mistake? Here's how belated, revised and updated returns work for AY 2026-27 — the dates, the ₹1,000–₹5,000 late fee, and the other penalties.

ELSS Funds: Save Tax + Grow Wealth

ELSS funds give you an 80C tax deduction, a 3-year lock-in and equity-linked returns. Here's how they're taxed, ELSS vs PPF, and whether they still make sense in the new tax regime.

How to Save Tax Beyond Section 80C

Maxed out your ₹1.5 lakh under Section 80C? Save more with 80D, the extra ₹50,000 NPS deduction, home loan interest and more — and see what still works in the new tax regime.